TL;DR

- Launching embedded payments is a major milestone, but it is only the beginning of the opportunity.

- Many vertical SaaS companies experience slowing merchant adoption after launch because they stop investing in the business of payments once implementation is complete.

- Industry research suggests that payments maturity, not simply years in market, is one of the strongest indicators of long-term success.

- The highest-performing software companies continue investing in merchant education, backbook conversion, customer marketing, operational optimization, and executive ownership long after go-live.

- Embedded payments should be managed like every other recurring revenue business inside your company, not like a completed implementation project.

Embedded payments have evolved from a convenient product enhancement into one of the most important strategic growth opportunities available to vertical SaaS companies. For many software providers, payments now influence recurring revenue, customer retention, product differentiation, and ultimately company valuation. It’s one of the few initiatives capable of increasing revenue from existing customers while simultaneously improving the overall customer experience.

Launching an embedded payments program has also become significantly easier. Modern APIs, hosted onboarding, and PayFac as a Service have dramatically reduced implementation complexity, making it possible for software companies of every size to bring integrated payments to market. As a result, more platforms than ever before are introducing embedded payments as part of their long-term product strategy.

Despite those advances, many software companies never achieve the adoption or recurring revenue they originally expected. The technology performs exactly as designed. Merchants begin processing payments. Revenue starts flowing. Then growth slows.

The reason usually isn’t technical. It’s operational.

According to Rainforest’s 2026 Vertical SaaS Embedded Payments Benchmarking Study, nearly 80% of software companies are targeting payment adoption rates above 70%, yet only about one-quarter have reached those goals. The same report found that companies offering embedded payments for five years don’t necessarily outperform organizations that launched much more recently. Payments maturity, not simply time in market, has become one of the strongest indicators of long-term success.

That finding closely mirrors what we’ve observed after helping software companies build and scale embedded payments businesses for more than twenty years. The organizations creating the greatest value aren’t necessarily those with the most sophisticated technology. They’re the ones that continue investing in their payments business long after implementation is complete.

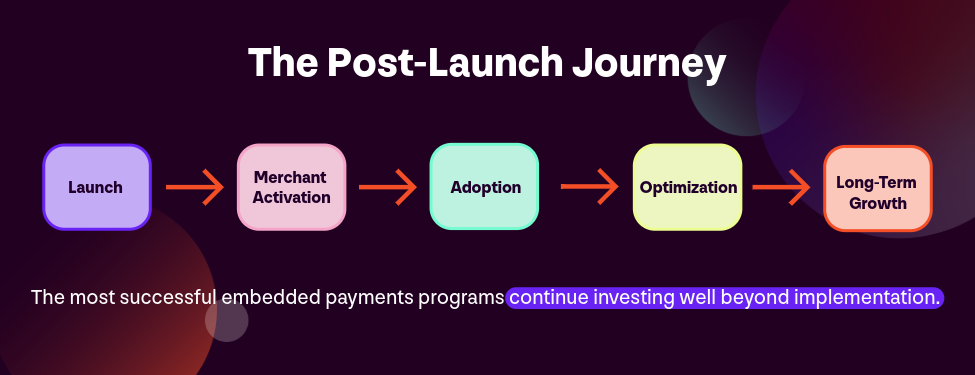

Launch Is Only the Beginning

Software companies instinctively understand that launching a new product feature is only the beginning of its lifecycle. Once a feature reaches the market, product teams continue refining the experience, marketing educates customers, sales improves messaging, and customer success works to increase adoption. Leadership reviews performance, studies customer feedback, and continually adjusts its strategy based on changing business priorities.

Embedded payments deserve the same level of attention.

Too often, however, software companies unintentionally treat payments as a completed implementation project instead of an ongoing business initiative. Once merchants begin processing, engineering moves to the next release, marketing returns its focus to the core platform, and leadership assumes the payments program will continue growing on its own.

Initially, everything appears to be working. Processing volume increases, merchants successfully complete onboarding, and recurring revenue begins appearing on executive dashboards. Six to twelve months later, leadership notices a different trend. Merchant adoption has slowed, existing customers continue processing with another provider, and attach rates have begun to level off.

At that point, many organizations immediately begin searching for product improvements. They consider redesigning onboarding, adjusting pricing, or introducing additional payment methods. While each of those changes can improve the customer experience, they rarely address the underlying issue.

The payments program stopped evolving.

The highest-performing software companies understand that implementation creates the opportunity, but commercialization creates the value. They continue investing in merchant education, customer communications, onboarding improvements, and operational excellence because they recognize that payments behave like every other recurring revenue business inside the organization.

Your Biggest Growth Opportunity May Already Be a Customer

Software executives naturally spend considerable time discussing new customer acquisition. Every SaaS company depends on expanding its customer base, entering new markets, and winning competitive deals. Embedded payments introduce another growth opportunity that often receives far less attention.

It’s the merchants who already trust your software.

Every customer processing payments through another provider has already chosen your platform. They’ve invested time implementing your solution, training employees, and building their daily workflows around your application. The opportunity isn’t convincing them to adopt your software. It’s helping them understand why processing payments inside your platform creates a better business.

A backbook conversion is one of the largest opportunities available to software companies seeking higher payment adoption. Yet many organizations unintentionally underestimate what successful a backbook conversion requires.

Merchants rarely switch payment providers because they receive a single announcement email. They change providers when they clearly understand the operational benefits of making that transition. They want to know how integrated payments improve reporting, simplify reconciliation, reduce manual work, accelerate funding, and create a better experience for both employees and customers.

Building that confidence requires more than a product announcement. It requires an intentional strategy that combines marketing, sales, customer success, onboarding, and executive sponsorship. Companies that continue communicating the value of integrated payments long after launch consistently outperform organizations that assume merchants will naturally migrate over time.

We’ve seen this approach create meaningful business results across multiple industries. One healthcare software company partnered with Xplor Pay after recognizing that implementation alone wouldn’t achieve its long-term payments goals. Leadership continued investing in merchant education, onboarding improvements, and customer communications after launch, helping transform payments from another product feature into a strategic growth initiative. The result was higher merchant adoption, stronger recurring payments revenue, and a payments program that continued growing long after implementation was complete.

→ Related: See how one healthcare software company transformed payments into a long-term growth strategy.

Every merchant who transitions to your payments program creates value far beyond the initial activation. Those individual conversions compound month after month, strengthening recurring revenue while making the software platform more valuable over time.

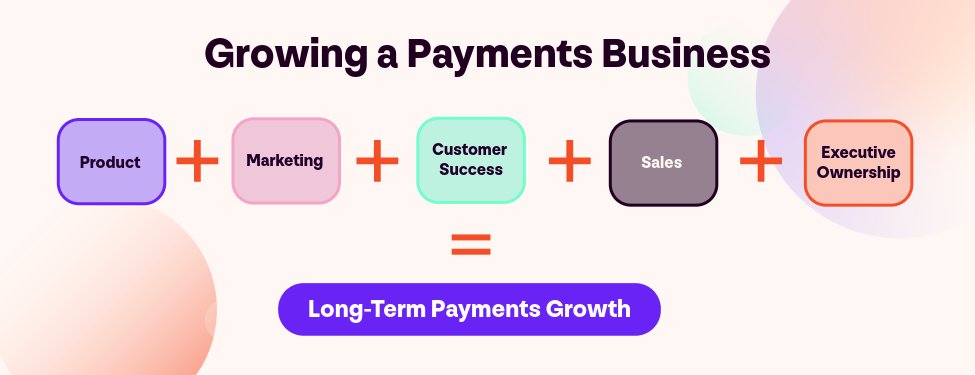

Merchant Adoption Is a Business Strategy, Not a Product Feature

One of the biggest misconceptions surrounding embedded payments is that adoption is primarily a product challenge. Product certainly matters. A confusing onboarding experience or poorly integrated workflow creates unnecessary friction and slows merchant activation.

Long-term adoption depends on much more than technology.

Successful software companies recognize that merchant adoption is the result of multiple teams working toward the same objective. Marketing educates customers about the value of integrated payments. Sales reinforces that message during customer conversations. Customer success helps merchants transition with confidence. Product teams continue improving workflows while leadership regularly reviews adoption metrics and identifies opportunities for improvement.

Organizations that align those functions create sustained momentum long after launch. Instead of relying on implementation alone, they build an operating model designed to increase adoption quarter after quarter.

That’s the difference between launching embedded payments and building a successful payments business.

Marketing Is What Turns Availability Into Adoption

Many software companies assume that once embedded payments are available, adoption will naturally follow. In reality, availability and adoption are two very different things. Merchants don’t switch payment providers simply because a new option appears inside the software. They switch because they understand how integrated payments will improve the way they operate their business and believe the transition will be worth the effort.

That requires far more than a successful implementation. It requires a deliberate strategy to educate merchants, reinforce value over time, and remove uncertainty throughout the customer journey. The highest-performing software companies continue investing in customer communications long after launch because they recognize that merchant education is an ongoing process, not a one-time campaign.

Successful adoption programs often include webinars, customer success stories, onboarding campaigns, implementation guides, in-product messaging, executive business reviews, sales enablement resources, and regular customer outreach. Every interaction reinforces why integrated payments create a better operational experience and why making the switch benefits both the merchant and their customers.

This is one of the areas where Xplor Pay has intentionally invested alongside its partners. Dedicated Partner Launch Managers help software companies prepare for a successful rollout, while our partner marketing team works collaboratively to build co-branded campaigns, merchant communications, webinars, and backbook conversion programs. Rather than ending the relationship at implementation, we continue helping partners increase merchant adoption and grow recurring payments revenue over time.

One partner simplified its onboarding process by introducing automated merchant onboarding, reducing friction for both merchants and internal teams while accelerating activation. Another paired its integration with ongoing merchant education and targeted customer outreach, creating sustained adoption instead of relying exclusively on new software sales.

The Best Software Companies Never Stop Optimizing

Every successful software company continually improves its product. Features evolve, workflows become more efficient, pricing adapts to market conditions, and customer feedback shapes future development. Those improvements rarely happen all at once. Instead, they accumulate over time and create a better experience for customers.

A successful payments strategy should evolve in exactly the same way.

The strongest software companies don’t simply ask whether embedded payments are working. They ask how it can work better. Leadership teams regularly review merchant adoption, onboarding completion, attach rates, payment mix, support requests, customer feedback, and operational efficiency. They identify opportunities to simplify reconciliation, introduce ACH, reduce friction, and improve reporting because they understand that small operational improvements compound over time.

Each enhancement creates a slightly better merchant experience. Better experiences increase adoption. Higher adoption generates additional recurring revenue. That recurring revenue creates additional resources to continue improving both the payments business and the software platform. Over time, those incremental improvements become a meaningful competitive advantage that is difficult for competitors to replicate.

We’ve seen this evolution firsthand. One restaurant technology provider initially launched embedded payments through a traditional integrated model. As the company grew, leadership recognized that greater ownership over the payments experience would better support its long-term vision. Rather than rebuilding its platform, the company transitioned to a PayFac as a Service model that aligned its payments strategy with the future direction of the business.

The lesson wasn’t simply that the company changed payment models. The lesson was that its payments strategy evolved alongside its software strategy.

Five Questions Every CEO Should Ask About Their Payments Business

Software executives routinely review recurring revenue, customer retention, product adoption, and sales performance. Embedded payments deserve the same level of executive attention. If your payments program has been live for more than six months, these questions can help determine whether it’s continuing to mature or beginning to plateau.

- Are we measuring merchant adoption or simply processing volume? Processing volume reflects where the business is today. Merchant adoption indicates how much opportunity remains for tomorrow.

- How many existing customers still process payments somewhere else? For many software companies, the largest payments opportunity already exists within the installed customer base.

- Who owns the long-term success of our payments business? If ownership becomes unclear after launch, continuous improvement often slows as other strategic priorities take precedence.

- When was the last time we actively marketed payments to our existing customers? Merchant adoption rarely happens automatically. Consistent education and communication remain essential long after implementation.

- Has our payments strategy evolved as quickly as our software strategy? As your company grows, your payments business should continue evolving alongside it.

Conclusion

Launching embedded payments is an important milestone, but it isn’t the destination. The software companies creating the greatest long-term value understand that implementation marks the beginning of a much larger opportunity. They continue investing in merchant education, customer marketing, onboarding, operational excellence, and continuous optimization because they recognize that payments behave like every other recurring revenue business inside the organization.

The most successful software companies don’t view embedded payments as another feature on the product roadmap. They operate it like a business within their business.

That mindset changes the conversations leadership teams have after launch. Instead of asking whether payments are working, they ask how adoption can improve, how more existing customers can be converted, how operational friction can be reduced, and how payments can contribute even more value to the overall business. Those organizations consistently outperform companies that assume growth will happen naturally after implementation.

Technology enables embedded payments. Execution creates enterprise value.

If your payments program launched a year ago, the most important question may no longer be “Did we launch successfully?” It may be “Have we continued building the business we set out to create?”

Frequently Asked Questions

Q. Why do embedded payments programs plateau after launch?

A. Most software companies shift their attention away from payments once implementation is complete. Without continued investment in merchant education, customer marketing, onboarding, and optimization, adoption naturally slows even when the technology performs well.

Q. What is backbook conversion?

A. Backbook conversion is the process of transitioning existing software customers from another payment provider to your embedded payments solution. For many software companies, it represents one of the largest opportunities to increase recurring payments revenue without acquiring new customers.

Q. Why is merchant adoption more important than processing volume?

A. Processing volume measures current activity. Merchant adoption measures how broadly customers have embraced your integrated payments offering and provides a stronger indicator of long-term growth.

Q. What role does marketing play after launch?

A. Marketing helps merchants understand the operational value of integrated payments through educational content, customer success stories, webinars, onboarding campaigns, sales enablement, and ongoing customer communications. Strong marketing programs are often one of the biggest differences between payments programs that plateau and those that continue growing.

Q. How often should software companies review their payments strategy?

A. Leadership should review payments performance as regularly as they review recurring revenue, customer retention, product adoption, and other strategic business metrics. As the software business evolves, the payments strategy should evolve alongside it.

Continue the Conversation

Embedded payments should deliver more than processing volume. It should strengthen customer relationships, create new recurring revenue, and increase the long-term value of your software business.

If you’re evaluating your current payments strategy or looking for new ways to improve merchant adoption after launch, we’d welcome the opportunity to share what we’ve learned after growing and scaling more than 20 vertical software platforms over the last 20 years.

by Xplor Pay

-

First published: June 30 2026

Written by: Xplor Pay