TL;DR

- Embedded payments are increasingly influencing retention, monetization, workflow ownership, and enterprise value.

- Transaction volume alone rarely tells the full story. Adoption, operational maturity, and workflow dependency often matter more.

- Many platforms stop at “payments enabled” and never fully operationalize payments across the business.

- Investors are increasingly evaluating embedded payments as part of broader diligence conversations.

- The strongest platforms treat payments as a strategic asset rather than a processing feature.

Why Embedded Payments Has Become an Investment Consideration

Two vertical SaaS companies can report nearly identical ARR, growth rates, and customer counts, yet one may ultimately prove far more valuable than the other.

The difference often comes down to factors that rarely appear in a traditional SaaS dashboard, including payment adoption, workflow ownership, operational maturity, and monetization depth.

For years, embedded payments were viewed primarily as infrastructure. A software company selected a processor, completed an integration, enabled payment acceptance, and moved on to the next initiative. During diligence, investors focused largely on product-market fit, recurring revenue, retention, growth, and market opportunity. Payments rarely played a meaningful role in the investment thesis.

That perspective is evolving.

As embedded payments become more deeply integrated into customer workflows, investors are increasingly evaluating how payments contribute to retention, monetization, operational scalability, and enterprise value. The question is no longer simply whether a platform offers payments. Investors want to understand how much strategic value payments create and how deeply they are embedded within the operating model of the business.

Vertical SaaS companies are particularly well positioned to benefit from this shift. Unlike horizontal software platforms, they often sit directly inside the day-to-day operations of their customers. Contractors collect deposits in the field. Healthcare platforms manage recurring patient billing. Automotive software processes transactions inside dealership workflows. Event platforms manage ticketing, registrations, and concessions.

In each case, payments become part of the workflow itself. As financial processes become more deeply integrated into the platform, customer dependency often increases, workflows become more centralized, and switching costs rise. What begins as a payment capability can evolve into a strategic business asset.

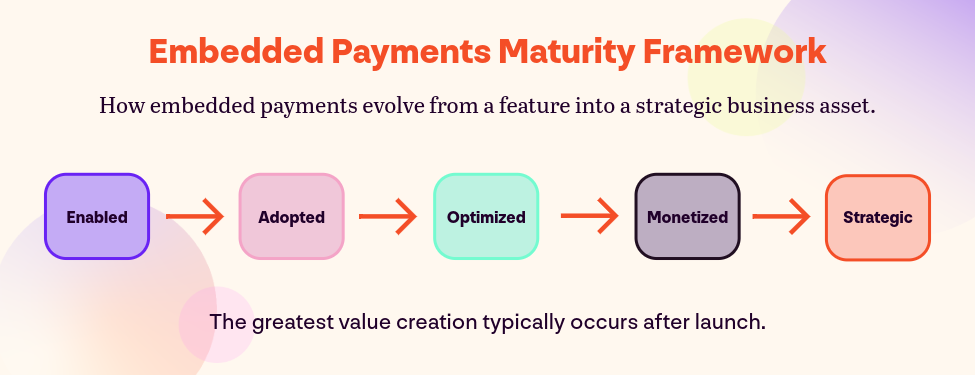

The Embedded Payments Maturity Framework

One of the most common mistakes investors make is evaluating embedded payments as a yes or no feature. Either a platform offers payments or it does not.

In reality, embedded payments typically evolve through several stages of maturity. Understanding where a company sits on that journey can provide valuable insight into current performance and future opportunities.

A platform that has merely enabled payments may generate processing volume. However, the strongest outcomes often emerge after organizations operationalize payments across onboarding, customer success, support, reporting, and product strategy.

As companies move through the maturity curve, payments often begin influencing broader business outcomes including customer retention, operational visibility, workflow ownership, monetization opportunities, and enterprise value.

This framework also helps explain why similar SaaS businesses can produce dramatically different outcomes from embedded payments despite using similar technology.

What Investors Often Miss During Diligence

Most embedded payments conversations begin with economics. Revenue share percentages, transaction volume, and monetization projections often dominate the discussion.

While those metrics matter, they rarely tell the complete story.

Many diligence processes overlook the operational factors that determine whether a payments program ultimately succeeds. Questions around adoption, onboarding, support readiness, reporting infrastructure, and organizational ownership frequently provide a more accurate picture of long-term value creation than transaction volume alone.

Transaction volume is particularly easy to misunderstand. It is highly visible, easy to measure, and often highlighted during diligence. Yet volume alone does not reveal how deeply payments are embedded into customer workflows or how broadly payments have been adopted across the customer base.

A platform processing hundreds of millions of dollars annually may have relatively low customer participation. Another platform with lower overall volume may have significantly stronger adoption, deeper workflow integration, and greater long-term strategic value.

This is why sophisticated investors increasingly look beyond volume and ask questions such as:

- What percentage of customers actively use payments?

- How has payments adoption changed over the last 12 months?

- What percentage of gross revenue flows through the platform?

- Where does onboarding friction occur?

- How long does merchant activation typically take?

- Who owns payments internally?

- How fragmented is the payments infrastructure?

- How dependent are customer workflows on payments?

- If payments disappeared tomorrow, how much customer value would disappear with them?

Collectively, these answers often provide a far clearer picture of long-term opportunity than transaction volume alone.

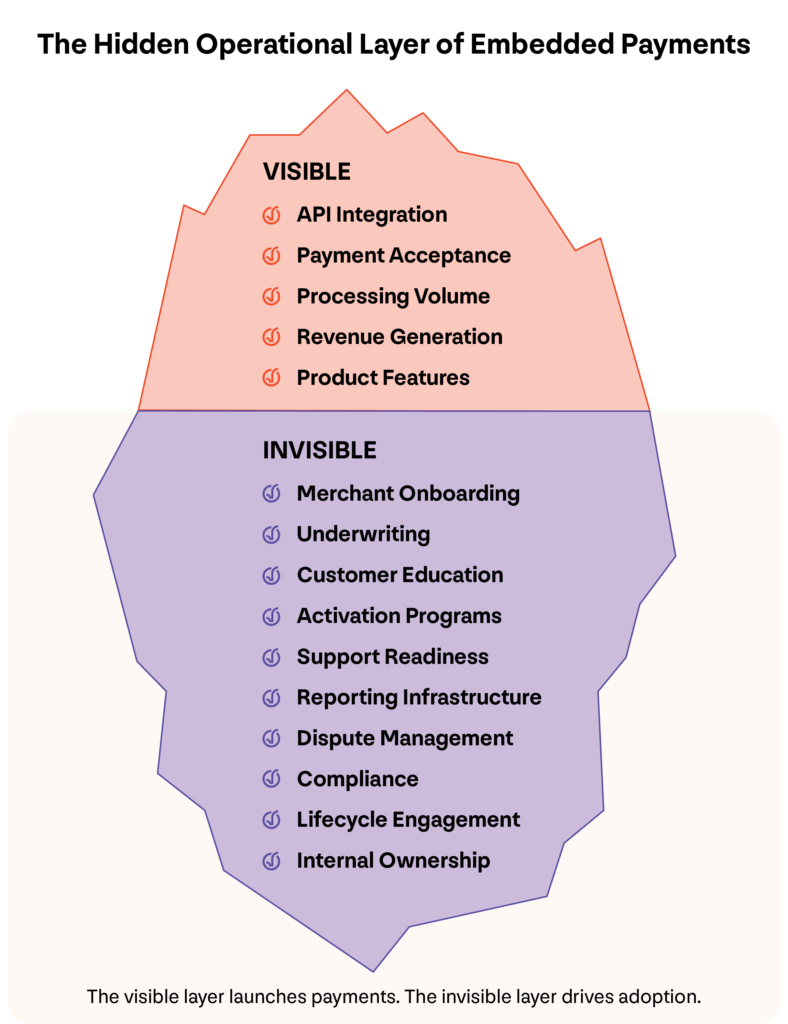

The Hidden Operational Layer of Embedded Payments

Many embedded payments programs succeed or fail based on operational factors that rarely appear in product demonstrations or executive summaries.

The visible layer is relatively easy to evaluate. Investors can review integrations, transaction volume, payment acceptance capabilities, and revenue generation. The invisible layer is more difficult to assess, yet it often determines adoption, scalability, and long-term performance.

The operational realities of embedded payments become even more apparent after launch. Many organizations assume that integrating payments will naturally lead to adoption. In practice, onboarding, activation, customer education, support readiness, and executive ownership often determine whether customers embrace the solution.

This is why launching payments and scaling payments are fundamentally different challenges.

The integration may be the most visible milestone, but it is rarely the most difficult. The real challenge begins when organizations attempt to drive adoption, remove operational friction, and scale payments across a growing customer base.

Organizations that treat payments as a cross-functional discipline involving product, operations, customer success, support, sales, finance, and executive leadership often produce significantly stronger outcomes than those that treat payments primarily as a product initiative.

What Operators Learn After Scaling Payments Across Multiple Platforms

One advantage of operating inside a company that has built and scaled more than 20 vertical SaaS platforms is the ability to observe payment adoption across a wide range of business models, customer bases, and growth stages.

Across those platforms, one pattern consistently emerges: the strongest payment outcomes rarely come from technology decisions alone.

The highest-performing platforms operationalize payments across onboarding, customer success, support, reporting, lifecycle communication, and executive ownership. Organizations that treat payments as a business discipline often outperform those that view payments primarily as a feature release.

This helps explain why companies with similar payment infrastructure can produce dramatically different adoption rates, retention outcomes, and monetization results.

It also explains why experienced operators tend to focus less on launch timelines and more on operational readiness. The question shifts from “How quickly can we integrate?” to “How effectively can we drive adoption and scale?”

The answer often determines whether payments become a modest revenue stream or a meaningful strategic asset.

Portfolio-Level Patterns Investors Start Seeing

As investors evaluate multiple software businesses across a portfolio, common patterns begin to emerge.

Different processors. Different onboarding experiences. Different support structures. Different reporting environments. Different monetization models.

The complexity often becomes even more pronounced following acquisitions.

What initially appears to be a payment infrastructure decision frequently turns into an operational challenge spanning multiple businesses. Fragmented payment environments can create inefficiencies, inconsistent customer experiences, limited visibility, and increased operational burden.

As a result, many investors begin evaluating payments differently. The conversation shifts from processing to scalability, from integration to adoption, and from infrastructure to enterprise value.

The most valuable insight is often not whether payments exist, but how effectively it is operationalized.

How Embedded Payments Influence Enterprise Value

The most successful vertical SaaS companies in your portfolio are increasingly viewing payments as part of the operating system of the business.

This perspective extends well beyond transaction revenue.

Embedded payments can influence customer retention, net revenue retention, revenue per customer, workflow dependency, operational visibility, forecasting accuracy, margin expansion, and long-term customer stickiness. As payments become more deeply embedded into customer operations, it often becomes more difficult to replace and more valuable to the business.

For investors, understanding payment economics is only part of the equation. The larger opportunity is understanding how deeply payments are embedded into customer workflows, how effectively they are operationalized, and how they contribute to long-term business performance within your portfolio.

The platforms creating the greatest value are rarely the ones that simply enabled payments. They are the ones that transform payments into a strategic asset that influences retention, monetization, operational leverage, and enterprise value.

Closing Perspective

For years, embedded payments was viewed primarily as infrastructure. Today, it is increasingly influencing how the vertical SaaS companies you invest in monetize, retain customers, scale operations, and create enterprise value.

As a result, embedded payments is becoming more than a product decision. It is becoming an operating model decision.

The investors and operators creating the most value are often the ones looking beyond transaction volume and payment economics. They focus on adoption, workflow ownership, operational maturity, and the role payments plays in the long-term durability of the business.

In many cases, the question is no longer whether a platform offers payments. The more important question is how effectively payments have been integrated into the company’s strategy for growth, retention, and value creation.

Frequently Asked Questions

Q. How do embedded payments impact enterprise value?

A. Embedded payments can influence retention, revenue per customer, workflow ownership, operational visibility, and customer stickiness. As payments become more deeply integrated into customer operations, they often become more difficult to replace and more valuable over time.

Q. What payment metrics matter beyond transaction volume?

A. Investors should evaluate payment adoption rates, workflow dependency, onboarding efficiency, operational scalability, reporting visibility, customer participation, and monetization flexibility.

Q. Why do some embedded payments programs underperform?

A. Many programs underperform because adoption never reaches its potential. Common causes include onboarding friction, weak activation processes, insufficient customer education, unclear ownership, and limited operational support.

Q. What is the difference between payments enabled and payments adopted?

A. Payments enabled means the technology has been integrated. Payments adopted means customers actively use payments as part of their day-to-day workflows.

Q. Why is payment adoption often more important than launch speed?

A. A platform with high adoption frequently creates more long-term value than a platform with aggressive economics and weak participation. Adoption is often a stronger indicator of strategic value than launch speed alone.

Q. Why are investors evaluating payments more closely during diligence?

A. Payments increasingly influence retention, monetization, workflow ownership, and enterprise value. Investors are looking beyond transaction volume to understand how deeply payments are embedded into the operating model of the business.

by Xplor Pay

-

First published: June 12 2026

Written by: Xplor Pay